Winning the distribution phase: How to efficiently access your money when you retire

- bryanjepson

- Nov 19, 2025

- 8 min read

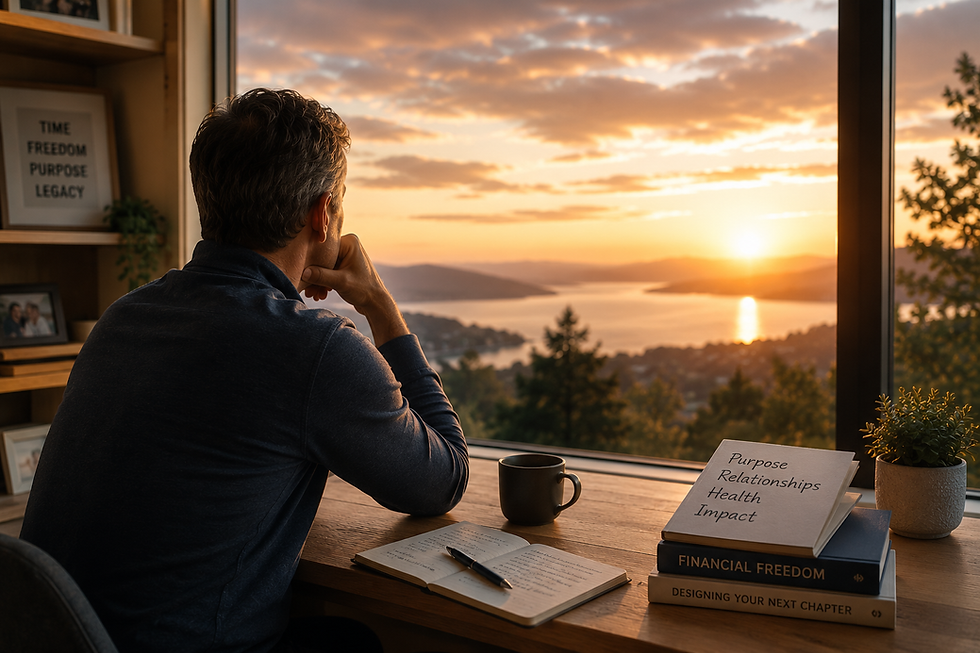

You’ve worked hard your entire career and made the right financial decisions to build a solid nest egg and to be positioned to retire on your own terms. But the accumulation phase in life is only half of the story. Now you have to start distributing and living off your assets. First, are you ready for that shift in mindset? It turns out that it is harder than you think. Second, do you know how to access your money in a logical and tax-efficient manner?

These are common questions that many physicians and other high-income professionals must face. Let’s break down what financial independence really means and then explore your options for creating a sustainable retirement paycheck.

This article is adapted from the first video in my new series with Medical Economics magazine, The Financial Checkup, where we explore practical personal-finance topics for physicians at each stage of their careers. You can check out the video here.

What does it mean to be Financially Independent?

Financial independence (FI) isn’t about a specific number—it’s about freedom. It’s the point at which money is no longer the reason you continue working. You may still choose to work, but the choice is yours.

In my book, The Physician’s Path to True Wealth, I define True Wealth as having complete control over your time, combined with the financial resources to create meaning and joy in your life. Money itself doesn’t create meaning; it’s simply a tool to help you live intentionally, support the people you love, and pursue what matters most.

Does FI mean you must retire?

Many of you have heard of the FIRE movement in personal finance and its various iterations. FI stands for financial independence. RE? Retire Early. If you subscribe to that philosophy and you achieve FI, are you failing if you chose to not retire, but to keep working? Not at all. It depends on why.

Are you still working because you just don’t feel like you can accumulate enough or can ever match your wants with your resources? Then you should probably reexamine what really makes you happy in life.

Or do you choose to continue working because your career adds value and meaning to your life and you enjoy making an impact. If so, absolutely—keep going.

The point is, if you are financially secure, the choice is now yours. The key is to remain productive, engaged, and purpose-driven, whether or not you continue clinical work.

The Saver’s Mindset

One thing that most people who achieve financial independence have in common is that they are really good at saving and investing. They have been disciplined during their accumulation phase and have been consistent in keeping to their good financial plan. For some that have a goal of FIRE as early in life as possible, aggressive savings and investing might even come at the expense of things that might have been more important at the time, like spending time with your children when they are young instead of working that extra shift, for example. Or enough time off to recharge your battery so you stay energized for a longer career. Don’t let FIRE burn up your future or your relationships.

But, even if you kept it all in perspective, you might find when you are standing at the top of the hill and looking down the other side that it is psychologically harder than you had anticipated to become a spender after 30 years of being a saver. So, planning a smooth transition isn’t just about the numbers in your accounts, but also about some shifts in psychology. That being said, the rest of this article talks about the financial side.

The Three Income Buckets

Your retirement income will come from three main “buckets,” each with different tax rules and withdrawal strategies.

Bucket 1: Taxable Accounts (brokerage accounts, cash, high-yield savings accounts, CDs, real estate investments, private funds, etc).

The size of this bucket will be quite variable among early retirees. If you had high enough income that you easily maxed out your tax-advantaged retirement accounts and still had money left over to save, this bucket could be quite large—maybe even your largest bucket. If that is the case, and you are retiring early, you have a lot of flexibility. There are no tax penalties to access this bucket early. You already paid taxes on the money that you put into that bucket. You can take it out at any time.

The main consideration is the tax treatment of any gains on your investments, as well as any income that those investments produce (like interest income or dividends). Capital gains taxes are due in any year that you sell your investments. Capital gains tax rates are different than income tax rates and have their own income limits. The current rates are either 0%, 15% or 20%. Interest income is taxed at ordinary income rates, and most dividends on US stocks (“qualified”) are taxed as capital gains.

Bottom line: draw from this bucket first. You are already paying taxes on the gains and there are no penalties for early withdrawal. You can set up income ladders or structured asset sales to generate consistent income and minimize or at least predict your tax burden.

Bucket 2: Tax-Deferred Accounts (pre-tax contributions to 401(k), 403(b), 457(b), Traditional IRAs)

For most of us, this will be our largest retirement bucket. These are our workplace or individual retirement accounts. When we invest in these accounts, you opt to not include the money as taxable income in that year. It grows tax-free until we remove the assets in retirement, at which point it is fully taxable as ordinary income. As physicians with high salaries, it makes sense to defer the taxes from a time in life when we are in a high tax bracket to when we expect to be in a lower tax bracket (after retirement.) That way, we are paying relatively fewer taxes on the same money.

But there are rules. First, you cannot access this money before age 59½ without a 10% penalty (with exceptions). And second, you are required to start taking the money out when you reach age 73 (switches to age 75 in 2033). This is referred to as a required minimum distributions (RMD) and is based on an IRS life expectancy table. Failing to take an RMD results in a 25% penalty which continues to accumulate if not corrected immediately. The government will be paid!

Bottom line: draw from this bucket next. It makes sense to allow the money to continue to grow tax-free as long as possible, until you eventually need to start taking it out. The largest the bucket, the larger the RMD associated with it, and a large RMD can even push you back into a higher tax bracket.

Bucket 3: Tax-Free Accounts (Roth IRA, Roth 401(k)/403(b))

The final bucket is for Roth money. This is money that you paid taxes on at the time that you invested it but put it in a qualified retirement account rather than a taxable account. In that setting, it is still allowed to grow tax-free (no capital gains tax) and you can distribute it tax-free (no ordinary income tax). Plus there are no RMDs required from Roth accounts. In other words, you pay taxes on it once and never again, and you can leave it in there as long as you want. (There are some exceptions and restrictions for money that is in the accounts for less than 5 years and before age 59 1/2).

Another great thing about Roth accounts is that unlike pre-tax retirement accounts, your heirs can inherit this money tax-free as well. In most cases, they just have to distribute it within 10 years.

Bottom line: use this money last. Let it continue to grow tax-free for as long as possible. But when you need it, it doesn’t count as income and you don’t owe more taxes on it. And if you don’t need it, your heirs will thank you.

The Early Retirement Problem: The 59½ Wall

Because of the rules related to qualified retirement accounts, accessing your money can be tricky if you want to retire early, unless you have a large enough taxable account. Withdrawals from tax-deferred accounts before age 59½ generally incur a 10% penalty.

What happens if you want to retire at 57, 55, or even 50?

Good news: You have several ways around the wall.

Strategies to Access Money Before Age 59½

Here are the practical, IRS-approved strategies physicians can use to fund early retirement without penalties.

1. Tap Your Taxable Brokerage Accounts

Remember, these are the most flexible dollars you have.

Benefits:

No age restrictions

No withdrawal penalties

Long-term capital gains rates (often lower than ordinary income)

High-income earners often overlook this bucket—but it creates the easiest and most tax-efficient early-retirement paycheck.

2. Use Your 457(b)

If you have a governmental 457(b), you can withdraw funds at any age, penalty-free, once you separate from service. These easily roll over into any other qualified retirement plan like a 401k or IRA. If you need some of the money to live on, you can cash it out without penalty but it will can’t as ordinary income in that year.

Non-governmental 457(b)s have different distribution rules and you will need to talk to HR or the plan administrator to understand exactly what they are. But, the IRS does not charge a 10% penalty on the withdrawal.

3. The Rule of 55

If you separate from your employer after the year you turn 55, the IRS allows penalty-free 401(k)/403(b) withdrawals from that employer’s plan.

Important caveat: You must leave the money in the employer-sponsored plan. Rolling it to an IRA eliminates this benefit. And just because the IRS lets you do it doesn’t mean that your 401k plan allows it. Check with HR or the plan administrator to see if this is an option for you.

4. 72(t) SEPP (Substantially Equal Periodic Payments)

This rule allows you to take penalty-free withdrawals from an IRA before 59½. BUT, once you start, you must continue taking the exact same payment for: Five years or until you reach 59½ — whichever is longer.

It’s rigid and requires precise calculation, but it’s a legitimate strategy for early retirees.

5. Use Your HSA Strategically

The HSA is the most tax-advantaged account in existence:

Tax-deductible going in

Tax-free growth

Tax-free withdrawals for medical expenses

If you’ve saved old medical receipts from any year, you can reimburse yourself at any time—even years later—and use that money as retirement income.

6. Traditional (Pretax) Accounts After Age 59½

Once you reach 59½, all pretax retirement accounts are fully accessible without penalty. Withdrawals count as ordinary income.

At age 73, RMDs begin, whether you need the money or not.

7. Roth IRA Flexibility

This is your "safety valve."

Roth contributions: Always accessible tax- and penalty-free. You’ve already paid taxes on it, so you can get it back whenever you want.

Earnings: Accessible tax-free only after:

The account has been open for 5 years, and

You are 59½ or meet another qualified event (death, disability, first-home purchase up to $10k)

8. Roth Conversion Strategy (Roth Ladders)

If you're planning early retirement, you can convert pretax dollars into Roth dollars each year after you retire—while you’re in a lower tax bracket. After five years, those converted amounts can be withdrawn tax- and penalty-free.

This requires planning but can dramatically reduce lifetime taxes by lowering your pre-tax RMDs and keeping you from bumping into a higher tax bracket.

The Big Picture: Build a Retirement Paycheck plan

The real goal is tax and access diversification. When your money is spread across taxable, tax-deferred, and tax-free buckets, you gain the ability to assemble a custom income stream each year:

Lower taxes

More flexibility

Better control of Medicare IRMAA brackets

Ability to smooth out RMD impact

Better estate outcomes

In other words:

Don’t just save aggressively. Save strategically.

The more intentionally you build your buckets now, the more freedom you'll have when you're ready to rewrite your life after medicine.

If you would be interested in helping us help you with your retirement income strategy, don’t hesitate to reach out at www.targetedwealthsolutions.com for a free exploratory consultation.

Disclaimer: the material in this blog post is intended for general educational purposes only and should not be considered specific financial advice. You should always consult with your personal financial advisor to see how it might fit within your personalized financial plan.

Comments