How to Turn Your Health Savings Account Into Tax-Free Retirement Income

- bryanjepson

- 20 hours ago

- 6 min read

I recently had a client who is approaching an early retirement ask me about the best way to handle their health savings account moving forward before Medicare kicks in. I thought it would be a useful and instructive blog post.

Health Savings Accounts (HSAs) can become one of the most tax-efficient tools available in early retirement and a potential source of future tax-free income.

The Triple Tax Advantages of Health Savings Accounts

HSAs are unique from a tax perspective. They are the only savings vehicle that allows pre-tax contributions, tax-free growth, and tax-free distributions if used for qualified expenses. That’s a triple tax-savings whammy right there! If you use it wisely, the HSA account gives you a lot of flexibility down the road.

The Rules

Eligibility

In order to be eligible to contribute to an HSA, you need to have an eligible high-deductible health care plan. These are widely available and usually offered as a choice by your employer. They are also available from private insurance or ACA-compatible health options.

The deductibles can be substantial, especially for families, which means more out-of-pocket exposure before insurance coverage fully kicks in. But the high deductible means that the monthly premiums are lower.

The idea is for you to invest the difference in premiums from a lower deductible plan into an HSA and let the market help you grow the account. They work the best for those with high income or a big enough emergency savings account who can absorb those yearly health care costs out of pocket. It is also best for those who are healthy and don’t have anticipated significant health care expenditures. If you are not, a regular lower-deductible plan might make more sense.

Contributions

The IRS sets a yearly contribution limit to an HSA plan. In 2026, the contribution limit is $4,400 for an individual and $8,750 for a family, with an additional $1,000 catch-up contribution allowed for each spouse after age 55.

When you hit age 65 and enroll in Medicare, you are no longer eligible to contribute to an HSA.

Once in the HSA account, there are usually two destination options: a cash account and an investment account.

The cash account will generate minimal interest, similar to a bank. But it is flexible. You will be given a debit card which you can use to pay for any health-care related expenses directly to the providers. These payments will come from the cash account. You can set limits on how much you want to keep in that part of the account to maximize your flexibility with the rest automatically flowing to the investment portion.

For the money you don’t anticipate needing in the near term, it is best to move that to the investment account. Here you will be given investment options similar to a company’s 401k account. The options are established by the HSA custodian and are usually a restricted list of mutual funds or preset strategies based on your risk tolerance.

The general strategy is to keep only enough cash for near-term expenses and move the remainder into investments so the account can compound tax-free over time. If your cash account runs low, you can sell investments and replenish it from the investment account portion.

Expenditures and Penalties

You can spend money from your HSA at any time for health-care related expenses. The definition is fairly broad and can include everything from doctor visits, prescriptions, and hospital bills to dental work, eyeglasses, hearing aids, mental health services, Medicare premiums, and many other qualified medical expenses. (The IRS maintains a detailed list of qualified medical expenses in Publication 502.)

As long as it is for a qualified expense, it is tax and penalty free. If it is not for a qualified expense and you are under the age of 65, the withdrawal is treated as ordinary income on taxes plus an additional 20% penalty! If you are older than age 65, the penalty is waived but you are still taxed at your regular income rate.

Using the rules to create tax-free income

One of the most powerful and underappreciated features of HSAs is that although withdrawals must eventually match qualified medical expenses, they do not have to occur in the same year as the expense itself. You just need to be able to match them in case of an audit.

In other words, if you keep your receipts for all the medical expenditures that you pay for with cash out of pocket over the years, you can reimburse yourself later for those expenses from your HSA account. For example, if you spend $5000 a year on medical expenses, but rather than using your HSA money, you just pay for it out of pocket and keep the receipts. Twenty years later, you can reimburse yourself $100,000 from the HSA completely tax-free.

And in the meantime, you have 20 years of tax-free growth on that investment. That’s pretty awesome. You just need to be sure that you are good at record-keeping.

Example

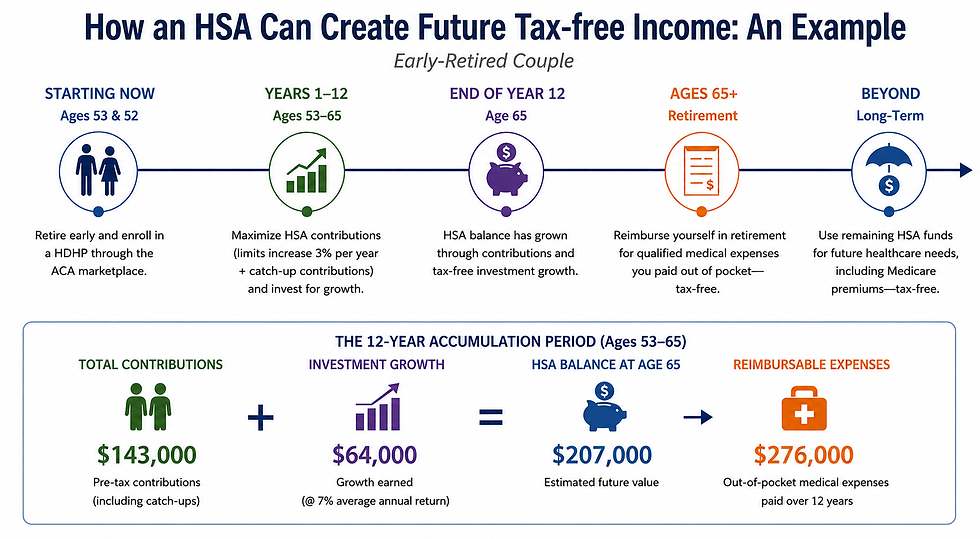

Now, let’s get to my client’s particular question. The specific numbers are all adjusted for for privacy sake. He plans on retiring early—at age 53. His wife is age 52. He has plenty in his taxable investment accounts to pay for any health care expenditures out of pocket and plans on getting a HDHP through the ACA portal. He has 12 years before he is eligible for Medicare.

Let’s say the health care premiums for his plan are $1500/month for he and his spouse. That is $18,000 per year just for the premiums.

Let’s say that other health care expenses total up to $5000 per year. That totals $23,000 annually.

Now here is his question: Should I start paying for health care now from my HSA plan or should I keep investing and pay out of pocket instead?

If we assume that the contribution limit increases every year by 3%, for the next 12 years, and that they both take advantage of the catch-up contributions, he and his wife could contribute pre-tax a total of around $143,000.

Now let’s assume that the investments grow at a conservative 7% per year. With those assumptions, his HSA will have grown by $207,000 over 12 years.

During that same time-frame, they have spent $276,000 in reimbursable health care expenses and have saved all of their receipts.

They anticipate spending about $150,000 per year in retirement living expenses. So, they could now live for almost 2 years, entirely income tax-free, if they choose to reimburse themselves from their HSA account.

Plus, investment growth alone covered roughly 75% of their cumulative reimbursable expenses during that period.

And after age 65, when they get Medicare and are no longer eligible for HSA contributions, they can use the remaining balance in their account to pay for Medicare Part B, Part D, and Medicare Advantage premiums tax-free. They should have enough in their account to pay for these extra healthcare costs for the rest of their lives. If there is money left over, they can reimburse themselves for prior expenses if they have the receipts, or just pay ordinary income tax without a penalty if they do not.

In this way, the HSA functions almost like a “stealth IRA”: tax deductions going in, tax-free growth along the way, and potentially tax-free income later in retirement.

Conclusion

If used strategically, an HSA can become much more than just a health-care spending account. It can serve as a long-term investment account, a reserve for future tax-free income, and a way to reduce the tax burden of retirement.

The key is patience and documentation. Pay medical expenses out of pocket when possible, save your receipts carefully, and allow the account to continue compounding in the background.

Years later, those receipts may become one of the most flexible sources of tax-free cash flow you have.

If you would like some help finding similar tax-savings strategies for your own financial situation, I'd love to hear from you. You can learn more about becoming a client at Targeted Wealth Solutions.

Disclaimer: the material in this blog post is intended for general educational purposes only and should not be considered specific financial advice. You should always consult with your personal financial advisor to see how it might fit within your personalized financial plan.

Comments